Fisheries and aquaculture in the Northeast Atlantic (Barents and Norwegian Seas)

This is Section 13.2 of the Arctic Climate Impact Assessment

Lead Authors: Hjálmar Vilhjálmsson, Alf Håkon Hoel; Contributing Authors: Sveinn Agnarsson, Ragnar Arnason, James E. Carscadden, Arne Eide, David Fluharty, Geir Hønneland, Carsten Hvingel, Jakob Jakobsson, George Lilly, Odd Nakken,Vladimir Radchenko, Susanne Ramstad,William Schrank, Niels Vestergaard,Thomas Wilderbuer

The potential impacts of climate change on the fisheries in the arctic area of the Northeast Atlantic are explored in this article. The area comprises the northern and eastern parts of the Norwegian Sea to the south, and the north Norwegian and northwest Russian coasts and the Barents Sea to the east and north. The fisheries are located in areas under Norwegian and Russian jurisdictions as well as in international waters. The total fisheries haul in the area were around 2.1 million t in 2001[1]. Aquaculture is dominated by salmon and trout and produced 86,000 t in 2001[2].

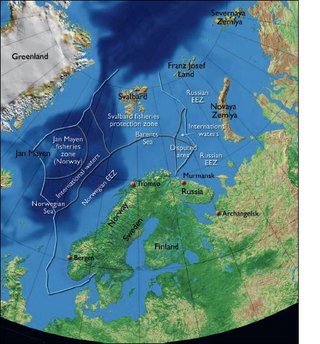

The legal and political setting of the fisheries in the Northeast Atlantic is complex. Norway and Russia established 200 nautical mile Exclusive Economic Zones (EEZs) in 1977, as a consequence of developments in international ocean law at the time. The waters around Svalbard come under a Fisheries Protection Zone set up by Norway, which according to the 1920 Svalbard Treaty holds sovereignty over the Svalbard archipelago. The waters around the Norwegian island of Jan Mayen, north of Iceland, are covered by a Fisheries Zone. Two areas occur on the high seas beyond the EEZs: in the Barents Sea the so-called “Loophole” and in the Norwegian Sea the so-called “Herring hole” (Fig. 13.2). Norway and Russia have long traditions of cooperation both in trade and management issues. In the 18th century, Norwegian fishermen in the north traded cod for commodities from Russian vessels – the so-called “Pomor-trade”[3]. Joint management of the Barents Sea fish stocks has been negotiated since 1975. Since then, a comprehensive framework for managing the living marine resources in the area has been developed, including the high seas. The resources in the area are exploited with vessels from Norway and Russia, as well as from other countries.

Northern Norway includes three counties: Finnmark, Troms, and Nordland, and covers an area of 110,000 square kilometers (km2) – about the same size as Great Britain. The total population is 460,000. Owing to the influence of the North Atlantic Current, the climate in this region is several degrees warmer than the average in other areas at the same latitude. While the Norwegian fishing industry occurs in many communities along the northern coast, the northwest Russian fishing fleet is concentrated in large cities, primarily Murmansk. In addition to the Murmansk Oblast, Russia’s “northern fishery basin” comprises Arkhangelsk Oblast, the Republic of Karelia, and Nenets Autonomous Okrug (see Fig. 13.2). There is no significant commercial fishing activity east of these regions until the far eastern fishery basin in the North Pacific. Since 1 January 2002, the population in the four federal subjects constituting Russia’s northern fishery basin was 3.2 million people.

Contents

- 1 Ecosystem essentials (13.2.1)

- 2 Fish stocks and fisheries (13.2.2)

- 3 Past climatic variations and their impact on commercial stocks (13.2.3)

- 4 Possible impacts of climate change on fish stocks (13.2.4)

- 5 The economic and social importance of fisheries (13.2.5)

- 6 Economic and social impacts of climate change on fisheries in the Northeast Atlantic (13.2.6)

- 7 Ability to cope with change (13.2.7)

- 8 Concluding comments (13.2.8)

- 9 References

- 10 Citation

Ecosystem essentials (13.2.1)

There are large seasonal variations in the upper water layers of the Barents Sea (see Section 9.2.4.1 (Fisheries and aquaculture in the Northeast Atlantic (Barents and Norwegian Seas))). The spring bloom starts in the southwestern areas and spreads north- and eastward following the retreat of the sea ice. Fish and marine mammals also exhibit directed migrations: spawning migrations south- and westward in late autumn and winter, and feeding migrations north- and eastward in late spring and summer.

Relatively few species and stocks make up the bulk of the biomass at the various trophic levels. Fifteen to twenty species of whales and seals forage regularly in the area. Harp seals (Phoca groenlandica) and minke whales (Balaenoptera acutorostrata) are the two most important predators in the pelagic ecosystem. The harp seals breed in the southeastern parts of the Barents Sea, i.e., in the White Sea, and feed close to the ice edge, mainly on amphipods and capelin. In periods of low capelin abundance, harp seals feed on other fish, such as cod, haddock, and saithe] (Pollachius virens), and migrate southward along the Norwegian coast[4]. Minke whales feed on various species of fish and over most of the area from May to September[5]. During the winter the whales occur further south in the Atlantic Ocean.

The spawning grounds of most species are situated along the coast of Norway and Russia. Spawning normally occurs in winter and spring (February to May) and egg and larval drift routes are toward the north and east. Juveniles and adults feed in the area; polar cod in the north- and northeasternmost parts, saithe and herring (Clupea harengus) in the southwest, as well as the easternmost Norwegian Sea and off the Norwegian coast. Capelin reside mainly on the Atlantic side of the Polar Front during winter, but feed on the zooplankton production in the large ice-free areas north of the Polar Front in summer and autumn. Cod has the most extensive distribution. Adult cod spawn in Atlantic water far south along the coast of Norway in March to April, and then feed along the Polar Front and even far into arctic water masses during summer and autumn. All species exhibit seasonal migrations, which coincide with the formation and melting of sea ice: north- and eastward during spring and summer, south- and westward during autumn and winter.

Cod, saithe, haddock, and redfish (Sebastes marinus and S. mentella) have their main spawning grounds on the coastal banks and off the shelf edge (redfish only) of Norway between 62º and 70º N and return to the Barents Sea after spawning. Herring migrate out of the Barents Sea before maturing, feed as adults in the Norwegian Sea, and have their main spawning grounds farther south along the Norwegian coast, between about 59º and 68º N. Capelin spawn in the northern coastal waters mainly between 20º and 35º E, while polar cod has two main spawning areas; one in Russian waters in the southeastern part of the Barents Sea and another in the northwest, close to the Svalbard archipelago. The capelin spawning schools are followed by predating immature cod, four to six years old. Adult Greenland halibut inhabit the slope waters at depths between 400 meters (m) and 1000 m over the entire area. Northern shrimp occur over most of the area in [[region]s] with bottom depths of between 100 and 700 m on the “warm” side of the Polar Front. Individuals are four to seven years old when they change sex from male to female and spawning (hatching of eggs) occurs in summer and autumn over most of the area.

From simulations of interactions among capelin, herring, cod, harp seals, and minke whales, Bogstad et al.[6] found the herring stock to be sensitive to changes in minke whale abundance because whale predation in the Barents Sea affects the number of recruits to the mature herring stock. They also found that an increasing harp seal stock will reduce the capelin and cod stocks, implying that an unexploited seal population would lead to a substantial loss of catch in the cod fishery.

Cod, capelin, and herring are considered key fish species in the ecosystem and interactions among them generate changes which also affect other fish stocks as well as marine mammals and birds[7]. Recruitment of cod and herring is enhanced by inflows of Atlantic water carrying large amounts of suitable food (especially the “redfeed” copepod Calanus finmarchicus) for larvae and fry of these species. Consequently, survival increases, so that juvenile cod and herring become abundant in the area. However, since young and juvenile herring prey on capelin larvae in addition to zooplankton, capelin recruitment might be negatively affected and thus cause a temporal decline in the capelin stock, an occurrence that would affect most species in the area (fish, birds, and marine mammals) since capelin is their main forage fish. Predators would then prey on other small fish and shrimps. In particular, cod cannibalism may increase and thus affect future recruitment of cod to the fishery[8].

In periods of low abundance or absence of capelin and/or herring, the top predators will have to feed somewhere else or shift to prey on the zooplankton group. For cod, such shifts have been observed twice in the past 15 years and were related to the collapses of the capelin stock in 1986–1988 and 1993–1994.

Fish stocks and fisheries (13.2.2)

For the past thousand years, fishing for cod and herring has been important for coastal communities in Norway and northern Russia[9]. Throughout the centuries, fishing was purely coastal and seasonal and based on the large amounts of adult cod and herring migrating into near-shore waters for spawning during winter–spring and on the schools of immature cod feeding on spawning capelin along the northern coasts in April to June. A certain development toward offshore fishing took place at the end of the 19th century when cod were caught on the Svalbard banks and driftnetting of herring began off northern Iceland. However, the quantities caught in these “offshore” fisheries were small compared to the near-shore catches in the traditional fisheries for both species. Estimates of annual yields of cod and herring prior to 1900 were given by Øiestad[10]. For both species large fluctuations were experienced. The dominant feature is the 5- to 10-fold increases between 1820 and 1880 as compared to yields in previous centuries. For fish species other than cod and herring reliable estimates of yield prior to the 20th century are not available.

Landings for herring, capelin, polar cod, Greenland halibut, northern shrimp, and northeast Atlantic cod in the 20th century are shown in Fig. 13.3. Total fish landings from the area increased from about 0.5 million t at the beginning of the century to about 3 million t in the 1970s. The increase was mainly due to a series of major technological improvements of fishing vessels and gear, including electronic instruments for fish finding and positioning, which took place during the 20th century and dramatically increased the effectiveness of the fishing fleet. Furthermore, there was a growing market demand for fish products.

Capelin

When herring became scarce in the late 1960s the purse seine fleet targeted capelin and catches increased rapidly in the 1970s. Management measures such as minimum allowable catch size and closing of areas where undersized fish occurred, as well as limited fishing seasons, were introduced in the early 1970s, first by Norway and later jointly by Norway and Russia. Total allowable catches (TACs) have been enforced since 1978. Landings have fluctuated widely. In 2002, the total catch of capelin was 628,000 t (Fig. 13.3). During the 1980s, the importance of capelin and juvenile herring as food sources for cod and other predators was fully realized[11]. As a consequence, there was increased research effort on species interactions and since 1990 the cod stock’s need for capelin as food has been taken into account in the scientific advice on management measures.

Polar cod

Russia and Norway started regular fisheries with bottom and pelagic trawls for polar cod in the late 1960s. The catches increased to approximately 350,000t in 1971. The Norwegian fleet was active until 1973, when fishers lost interest because of declining catches. Since then landings have been exclusively Russian. Catches in 2001 were about 40,000t.

Greenland halibut

Until the early 1960s, the Greenland halibut fishery (Fig. 13.3) was mainly pursued by coastal longliners off the coast of northern Norway. Annual landings were about 3,000t. An international trawl fishery developed in the area between 72º and 79º N and catches increased to about 80,000t in the early 1970s. Landings decreased throughout the 1970s; the spawning stock biomass declined from more than 200,000t in 1970 to about 40,000t in the early 1990s and has since remained at this low level. Since 1992, only vessels less than 28m in length using long lines or gillnets have been permitted to carry out a directed fishery. The rest of the fishing fleet has been restricted by by-catch rules. The total catch in 2002 was 13,000t.

Northern shrimp

Prior to 1970, trawling for northern shrimp took place in the fjords of northern Norway and catches were low. During the 1970s offshore grounds were exploited. Catches increased until 1984 when 128,000t were landed. Since then, catch levels have fluctuated (Fig. 13.3). Fisheries have been regulated by bycatch rules and closed areas since the mid-1980s. Areas are closed to fishing when the catch rates of young cod, haddock, and Greenland halibut exceed a certain limit. In later years, young redfish has also been included in the bycatch quota. Areas are also closed when the proportion of minimum-size shrimp (15 mm carapace length) is too high. In the Russian EEZ an annual TAC is also enforced. Estimated cod consumption of shrimp has since 1992 been approximately ten times higher than the landings, which were about 58,000t in 2001.

Herring

Until the 1950s, herring fisheries remained largely seasonal and near shore. The bulk of the landings came from Norwegian vessels. In the 1950s Russian fishers developed a gillnet fishery in offshore waters in the Norwegian Sea, and in the early 1960s purse seiners started using echo sounding equipment to locate herring. These technological developments resulted in a large increase in the total catches until 1966 (2 million t). Thereafter, catches decreased rapidly and the stock collapsed (Fig. 13.3 and Box 13.1). Although individual scientists expressed concern about the stock, effective management measures were neither advised nor implemented until after the stock had collapsed completely. Minor catches in the early 1970s (between 7,000 and 20,000 t) removed most of the remaining spawning stock as well as juveniles and it was not until 1975 that the fishing pressure was brought to a level which permitted the stock to start recovering. For 25 years the stock was very small and remained in Norwegian coastal waters throughout the year. Norway introduced management measures including minimum allowable landing size and annual TACs. Furthermore, a complete ban on fishing herring was enforced for some years. During the 1990s the stock recovered, started to make feeding migrations into the Norwegian Sea, and catch quotas and landings increased. In 2002 the total landings were 830,000t.

|

Box 13.1.The fall and rise of the Norwegian spring-spawning herring In the early 1950s, the spawning stock of Norwegian spring-spawning herring was estimated at 14 million t – one of the largest fish stocks in the world. Most of the adult stock migrated between Norwegian and Icelandic coastal waters to spawn in winter and feed in summer, respectively.The herring fishery was important for several countries, especially Norway, Iceland, Russia, and the Faroe Islands. However, after 15 years of overexploitation and a decreasing spawning stock, the stock collapsed in the late 1960s. Deteriorating climatic conditions north of Iceland and in the western Norwegian Sea are crucial in explaining changes of feeding areas and migration routes of these herring in the late 1960s. High fishing intensity was, however, the major factor behind the actual stock collapse.The breakdown had large social and economic consequences for those depending on the fishery. Nevertheless, the industry managed to redirect its effort to other pelagic species – primarily capelin. Over the following decades, the remaining herring kept close to the Norwegian coast.The stock was strictly regulated and fishing was prohibited for several years.These regulations, probably in combination with favorable climatic conditions, contributed to a considerable increase in stock size from the mid-1980s, making it possible to resume fishing. By the late 1980s the spawning stock had reached a level of 3 to 4 million t, mainly due to above average recruitment by the 1983 year class. By 1995, the spawning stock had reached 5 million t. As a consequence, the stock extended its feeding grounds by resuming its old migration pattern westward into the Norwegian Sea. It therefore became available for fishing beyond areas under Norwegian jurisdiction.The unilateral Norwegian management regime was no longer adequate to regulate fishing of the stock. Meanwhile, there was no arrangement to oversee the international management of the fishery. Negotiations between Norway, Russia, Iceland, and the Faroe Islands failed, and the total catch quota recommended by ICES was exceeded in the following year. High economic values were at stake for all actors. Fishers and fisheries managers in all involved countries and in the EU were very engaged in the conflict. A first agreement was reached between Norway, Russia, Iceland, and the Faroe Islands in May 1996. In December 1996, the EU was included in the arrangement, where the five parties set and distribute TACs of Norwegian spring-spawning herring, based on ICES advice.The responsibility to manage the share of the stock in international waters is vested with the NEAFC, of which the aforementioned parties are members. Negotiations are held every year, but the percentage allocation key has not changed since the 1996 agreement. However, changes in the migration pattern may upset the present arrangement. The arrangement is, however, not currently functional due to disagreement over quota distribution. This example shows that not only negative, but also positive changes in stock abundance may create management problems. If the parties had not reached agreement, there would have been devastating consequences for the exploitation and development of the Norwegian spring-spawning herring stock, almost certainly resulting in significant economic losses.This example shows the importance of political efforts to solve such conflicts. |

Northeast Atlantic cod

Prior to 1920, the bulk of the northeast Atlantic cod (Gadus morhua) catch was from two large seasonal and coastal fisheries: the fishery for immature cod feeding on spawning capelin along the northern coast of Norway and Russia and the fishery for spawning cod (“skrei”) further south off northern Norway (the Lofoten fishery). In the 1920s and 1930s an international bottom trawl fishery targeting cod as well as other species (haddock, redfish) developed in offshore areas of the Barents Sea and off Svalbard. Annual catches increased from about 400,000t in 1930 to 700,000 to 800,000t at the end of the decade. Landings also remained high after the Second World War until the end of the 1970s when catches declined sharply due to reduced stock size and the introduction of [[EEZ]s]. Management advice was given by the International Council for the Exploration of the Sea (ICES) from the early 1960s. Increases in trawl mesh sizes were recommended in 1961 and in 1965 a variety of further conservation measures were recommended in order to increase yield per recruit and to limit the overall fishing mortality. From 1969 onward, ICES has expressed concern about the future size of the spawning stock, considering that at low levels of spawning stock biomass there would be an increased risk of poor recruitment to the stock. The first TAC for cod was set in 1975, but was far too high. Although minimum mesh size regulations had been in force for some years at that time, it is fair to conclude that no effective management measures were in operation for demersal fish in the area prior to the establishment of 200nm EEZs in 1977.

The estimated average fishing mortality for the five year period 1997 to 2001 is a record high (0.90) and about twice the fishing mortality corresponding to the precautionary approach (0.42). In the period 1998 to 2000 the spawning stock biomass was well below the recommended precautionary level of 500,000t. However, despite relatively low recruitment in most recent years, the spawning stock has increased since 2000 and is now considered to be above precautionary levels. Landings have varied considerably over time and in 2002 were 430,000t (Fig. 13.3).

Marine mammals

Three species of marine mammals are commercially exploited in the Northeast Atlantic by Norwegian and Russian fishers, i.e., minke whales, hooded seals (Cystophora cristata), and harp seals. In addition, grey seals (Halichoerus grypus) and harbour seals (Phoca vitulina) are exploited along the Norwegian coast by local hunters. Offshore exploitation of marine mammals in the area began in the 16th century. Basque and later Dutch and British vessels hunted Greenland right whale (Balaena mysticetus) and seals. Processing plants were established at shore stations as far north as northwestern Spitzbergen[12]. Russian and Norwegian hunters have caught walrus (Odobenus rosmarus), polar bear (Ursus maritimus), and seals at the Svalbard archipelago since the 16th century. By the first decades of the 19th century the stocks of right whales had almost disappeared, and the walrus was so depleted that the hunt became unprofitable. A new era of offshore exploitation began around 1860 to 1870 when the use of smaller ice-going vessels (“sealers”) permitted Norwegian hunters to penetrate into the drift ice. At about the same time the invention of the grenade harpoon made hunting of great whales profitable. Catches of great whales increased between 1870 and 1900, but leveled off and decreased rapidly during the first decade of the 20th century.

Minke whales

Minke whales have been hunted in landlocked bays (“whaling bays”) along the coast of Norway since olden times. Offshore hunting, using small motorized vessels, developed prior to the Second World War, essentially as an extension of fishing activities. Catches increased until the 1950s, the mean annual take at that time being about 2300 animals. Since 1960, catches have decreased due to reductions in annual TACs. Between 1987 and 1992 no commercial hunting was allowed. In recent years annual catches have been 400 to 600 animals and the quota for 2002 is 674 minke whales. The stock in the area is estimated at 112,000 animals[13].

Harp seals and hooded seals

Two stocks of harp seal, in the West Ice (Greenland Sea) and the East Ice (White Sea – Barents Sea), and one stock of hooded seal in the West Ice are subject to offshore sealing; since about 1880 mainly by Norwegian and Russian hunters. The total annual catch from these stocks increased from about 120,000 animals around 1900 to an average of about 350,000 per year in the 1920s. Since then catches have declined, mainly because of catch regulations (i.e., TACs). In recent years the loss of [[market]s] has been the main limiting factor. In the 1990s, catches of harp seal in the West Ice were 8,000 to 10,000 animals each year and 8,000 to 9,000 for hooded seal, while catches of harp seal in the East Ice ranged from 14,000 to 42,000 per year. Russian catches, which constitute about 82% of the total, are taken in the East Ice, while the Norwegian catches (about 18%) are taken in both the West Ice and East Ice.

Hooded seals are found in the North Atlantic between Novaya Zemlya, Svalbard, Jan Mayen, Greenland, and Labrador. All the Norwegian catch of hooded seal takes place in the West Ice (Greenland Sea). Russia has not caught hooded seals since 1995. The total catch in 2001 was 3,820 animals. All seal stocks are assessed every second year by a joint ICES/NAFO (International Council for the Exploration of the Sea/ Northwest Atlantic Fisheries Organization) working group, which provides ICES with sufficient information to give advice on stock status and catch potential. All three stocks are well within safe biological limits, and harvesting rates are sustainable.

Past climatic variations and their impact on commercial stocks (13.2.3)

The relationship between the physical effects of climate change and effects on the ecosystem is complex. It is not possible to isolate, let alone quantify, the effects of climate change on biological resources. The following discussion is therefore of a tentative and qualitative nature.

A number of climate-related events have been observed in the Northeast Atlantic fisheries (see Section 9.3.3.3 (Fisheries and aquaculture in the Northeast Atlantic (Barents and Norwegian Seas))). During the warming of the Nordic Seas between 1900 and 1940, there were substantial northward shifts in the geographical boundaries for a range of marine species from plankton to commercial fish, as well as for terrestrial mammals and birds[14]. Recruitment of both cod and herring is positively related to inflows of Atlantic waters to the area and thus to temperature changes. Both stocks increased significantly between 1920 and 1940 when water temperatures increased[15]. The increase in stock size was probably an effect of enhanced recruitment, because catches increased in the same period. A similar development may have occurred between 1800 and 1870[16]. Øiestad[17] also provided evidence that cod abundance was low during the cold period between 1650 and 1750.

Since the Second World War both cod and herring have been subject to overfishing. This resulted in a collapse of the herring stock in the 1960s, with serious consequences for other inhabitants of the ecosystem as well as man. For cod, the most likely result of the overfishing has been a far lower average annual yield since 1980 than the stock has potential to produce. Recruitment of cod depends heavily on parent stock size in addition to environmental factors[18]. For several decades heavy fishing pressure has prevented maintenance of the cod spawning stock at a level which optimizes recruitment levels in the long run. Therefore, management of these stocks is the key issue in assessing the effects of potential climate variations[19].

Possible impacts of climate change on fish stocks (13.2.4)

Global models project an increase in surface temperature in the Northeast Atlantic area of 3 to 5ºC by 2070 (see Chapter 4 (Fisheries and aquaculture in the Northeast Atlantic (Barents and Norwegian Seas))). Regional models however, project that for surface temperatures in this area there will be “a cooling of between 0 and -1 ºC” by 2020[20]. By 2050 the area is projected to have become warmer and by 2070 surface temperatures are projected to have increased by 1 to 2 ºC[21].

Research over the last few decades shows that cod production increases with increasing water (Seawater) temperature for stocks inhabiting areas of mean annual temperature below 6 to 7 ºC, while cod stocks in warmer waters exhibit reduced recruitment when the temperature increases[22]. The mean annual ambient temperature for northeast Atlantic cod is 2 to 4ºC (depending on age group) and the stock has experienced greatly improved recruitment during periods of higher temperature in the past[23]. A rise in mean annual temperature in the Barents Sea over the period to 2070 is therefore likely to favor cod recruitment and production, and result in an extended distribution area (i.e., spawning and feeding areas) to the north and east. A similar statement may be made for herring (see Chapter 9 (Fisheries and aquaculture in the Northeast Atlantic (Barents and Norwegian Seas))). This statement is based on the assumption that the production and distribution of animals at lower trophic levels (particularly copepods – the food for larvae – remain unchanged. The projection is also based on the assumption that harvest rates are kept at levels that maintain spawning stock biomass above the level at which recruitment is adversely affected.

Experience indicates that it is likely that a rise in water temperature, as projected for the area, will result in large displacements to the north and east of the distribution ranges of resident marine organisms, including fish, shrimps, and marine mammals. Their boundaries are very likely to be extended as [[water (Seawater)]s] get warmer and sea-ice cover decreases. “Warm water” pelagic species, such as blue whiting (Micromesistius poutassou) and mackerel (Scomber scombrus), are likely to occur in the area in higher concentrations and more regularly than in the past. Eventually, these species will possibly inhabit the southwestern parts of the present “arctic area” on a permanent basis.

The effects of a temperature rise on the production by the stocks of fish and marine mammals presently inhabiting the area are more uncertain. These depend on how a temperature increase is accompanied by changes in ocean circulation patterns and thus plankton transport and production. In the past, recruitment to several fish stocks in the area, cod and herring in particular, has shown a positive correlation with increasing temperature. This was due to higher survival rates of larvae and fry, which in turn resulted from increased food availability. Food is transported into the area via inflows of Atlantic water, which have also caused the ocean temperature to increase. Hence, high recruitment in fish is associated with higher water temperature but is not caused by the higher water temperature itself[24].

Provided that the fluctuations in Atlantic inflows to the area are maintained along with a general warming of the North Atlantic [[water (Seawater)]s], it is likely that annual average recruitment of herring and cod will be at about the long-term average until around 2020 to 2030. This projection is also based on the assumption that harvest rates are kept at levels that maintain spawning stocks well above the level at which recruitment is impaired. How production will change further into the future is impossible to guess, since the projected [[temperature]s], particularly for some of the global models, are so high that species composition and thus the interactions in the ecosystem may change completely.

The economic and social importance of fisheries (13.2.5)

The fishery sector is of considerable economic significance in Norway, being among the country’s main export earners. Data used in this section are based on statistics from “Fisken og Havet” and the Norwegian Directorate of Fisheries, and include landings from catches taken in ICES statistical areas I, IIa, and IIb. In 2001, the export of fish products accounted for 14% of the total exports from mainland Norway (based on data from the Statistical Yearbook of Norway and information from the Norwegian Seafood Exports Council). The fisheries constituted 1.5% of the Norwegian Gross National Product in 1999, excluding petroleum. In northwest Russia, fisheries are of less economic importance nationally. A substantial share of the catches taken in Russian fisheries in the north is landed abroad.

Most northern coastal communities are heavily dependent on the fisheries in economic terms, as well as being culturally and historically attached to fisheries. As early as AD 1000 an extensive trade in dried cod had developed in northern Norway, through the Hanseatic trade[25]. The coastal fishery and trade made up the economic foundation for the communities along the northern coast. Since the early 1980s, aquaculture has become increasingly important, accounting for a significant part of the economic value of the fisheries sector[26].

The total fishery in the arctic Northeast Atlantic yields about 2.1 million t and has a total annual value of around US $2 billion. The resources occurring in the Arctic are also significant to fishery communities elsewhere. A substantial component of the catches in the Arctic is taken by fishers from outside the region, such as those from southern Norway and elsewhere in Europe.

Fish stocks and fisheries

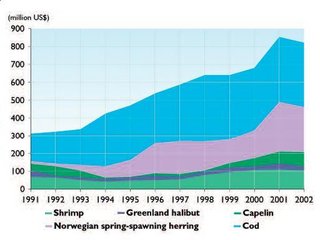

Fig. 13.4. Nominal value of the landings in Norway from the arctic fisheries, 1991–2002 (data from the Fisheries Directorate, Bergen, Norway).

Fig. 13.4. Nominal value of the landings in Norway from the arctic fisheries, 1991–2002 (data from the Fisheries Directorate, Bergen, Norway). Most of the Norwegian fish harvest is taken in the Norwegian EEZ (Fig. 13.2). Altogether, the waters under Norwegian jurisdiction cover around 2 million km2 – more than six times the area of mainland Norway. The arctic fisheries occur in three main areas: the Barents Sea/Svalbard area, the north Norwegian coast, and around Jan Mayen

In the Norwegian fisheries, northeast Atlantic cod is by far the most important stock in economic terms. The landed value was approximately US $350 million in 2000, but had declined to just below US $209 million in 2002 (Fig. 13.4). The landed value of herring also increased considerably throughout the 1990s, to about US $205 million in 2002. The third most valuable species is northern shrimp, of which the landed value was approximately US $100 million in 2000, but had declined to about US $85 million by 2002. Other important fisheries include those for capelin, Greenland halibut, king crab (Paralithodes camtschaticus), haddock, and saithe. These fisheries are important to the processing plants along the coast, and so to the viability of coastal communities.

For the northwest Russian fishing fleet, northeast Atlantic cod is also the most important fish stock. Catches are taken in Russian as well as Norwegian waters. Since the early 1990s, most of the cod caught by Russian fishers in the Barents Sea has been landed abroad, primarily in Norway. Only small quantities of mainly pelagic fish have been landed in Russia from the Barents Sea in recent years. The share of the total catch from the Northeast Atlantic has however increased. The northwest Russian fishing fleet, previously engaged mainly in distant water fishing, now works in the immediate northern vicinity. While only 234,000 t were taken in the Northeast Atlantic in 1990, catches have been over 500,000 t in all years since.

The economic value of the commercial exploitation of marine mammals in Norway and Russia is of minor direct significance nationally and regionally. But since marine mammals are major consumers of commercial fish species, their harvest is seen as an important contribution to maintaining a balance in the ecosystem. The marine mammal fishery also has a long tradition. Archeological excavations and early historical records clearly show that whaling has been conducted since ancient times and that whales were exploited before AD 1000[27]. In the 17th century, British and [Holland|Dutch]] whalers killed an annual average of 250 Greenland right whales in the arctic and subarctic [[region]s]. These whales were processed at shore stations along the west coast of Spitsbergen[28].

Fishing fleets and fishers

The fishing fleet in northern Norway consists of around 1250 vessels operating on a year-round basis[29]. More than half are small vessels of 13m or less. The fleet has been considerably reduced since the early 1970s. Small vessels fishing with conventional gear such as nets, lines, and jigs dominate. A large part of the fishery therefore occurs close to shore and in the fjords. Larger coastal vessels are ocean going. Trawlers and purse-seiners dominate the offshore fisheries. The vessels are required to carry a license to fish, and also need a fish quota to be admitted to a particular fishery. There are almost no open access fisheries in Norwegian waters. Most coastal communities have a number of vessels attached to them.

Northwest Russian fisheries include a variety of fishery-related activities and participants. They are based in Murmansk and Arkhangelsk Oblasts, and in the Republic of Karelia[30]. Most of the activity is located in the city of Murmansk, where most vessel owners, fish processing plants, and management authorities have their premises. The association of fishing companies in “the northern basin” of the Soviet Union, Sevryba (“North Fish”), was founded in 1965 and given the status of General Directorate of the Soviet Ministry of Fisheries in Northwestern Russia. Sevryba was made a private joint-stock company in 1992. The majority of the approximately 450 fishing vessels located in northwestern Russia are controlled by a handful of fishing companies (referred to henceforth as the “traditional” companies). The rest are distributed between kolkhozy (fishing collectives) and private fishing companies (referred to henceforth as the “new” companies). The total number of vessels has been stable since the early 1990s: few old vessels have been taken out of service and few new vessels have been purchased[31].

The “traditional” fishing companies are a legacy from the Soviet period. This fleet mainly consists of medium-sized (50 to 70m) and large (over 70m) vessels, and has around 250 to 300 ships. Before the dissolution of the Soviet Union, their main activity was the exploitation of pelagic species in distant waters and fisheries in the northern Atlantic Ocean. These companies now deploy a fleet of mid-sized factory trawlers for fishing and processing codfish. The collective fleet is significantly smaller in number, with some 80 to 100 vessels. Nearly all are of medium size (50 to 70m). The fishing collectives are more diversified than other companies. Like the traditional companies, the collectives also aim at upgrading their fleet. The “new” companies (including the so-called coastal fishing fleet) have the smallest fleet, both in number and vessel size, limiting the range of the vessels and so the [[market]s] for the sale of the fish. The fleet comprises around 100 vessels, including around 30 coastal fishing vessels of less than 50m in length.

The Russian perception of “coastal fishing” differs from that in neighboring countries. While a Norwegian “coastal” fishing vessel normally has a small crew and goes to port for daily delivery of catches, a northwest Russian “coastal” fishing vessel has a crew of more than a dozen and stays at sea for weeks before landing the catch. The reasons for this are two-fold. The fishing industry that was developed during the Soviet period was based on large-scale fishing and processing. Traditions, skills, and infrastructure for small-scale coastal fisheries are therefore non-existent in the main fishing regions of the Russian Federation. In addition, fish stocks for developing a viable coastal fishery are not available. Also, the financial status of the fishing companies is an obstacle to the development of coastal fisheries[32].

The land side of the fishing industry

More than 90% of the fish landed in Norway – by Norwegian, Russian, and other countries’ vessels – is exported. Changes in the international market for fish and fish products may thus have substantial effects on the processing plants as well as on the rest of the industry. Many fish processing plants are heavily dependent on landings by Russian vessels. In 2001, around 70% of the Russian cod quota was landed in Norway. This percentage has since decreased, with the increase in landings in other countries and trans-shipments in the open ocean. The fishing industry, especially the fillet-producing plants, has experienced low profitability and an increasing number of bankruptcies in recent years[33]. Increased competition for raw materials and high production costs in Norway help to explain the problems. In addition, the advantage of the Norwegian industry has been its location near the resources. New freezing and defrosting technologies, and infrastructure developments that make frozen products more valuable[34], reduce the advantage of proximity to the resource.

There are around 170 fish processing plants in northern Norway[35]. The size of the plants varies substantially. Most are engaged in producing traditional whitefish products, for example dried cod, salted fish, and stockfish. In Finnmark, a relatively large proportion of the plants concentrate on fillet production, while the shrimp industry is more important in Troms[36]. In Nordland, both fillet and traditional production is important.

Before the dissolution of the Soviet Union, Murmansk had the largest fish processing plant of the entire Union. Since fishing in distant waters has been reduced and catches from northern waters landed abroad, activities at the fish processing plants in Murmansk have been drastically reduced. The production of consumer products fell from 83,300 t in 1990, to 10,100 t in 1998[37]. Processing of fish outside Murmansk is insignificant.

Aquaculture

Since around 1980, Atlantic salmon (Salmo salar) and trout (Oncorhynchus mykiss)-based aquaculture has developed in Norway, making this country the world’s biggest farmed salmon producer. Total production in 2000 was 485,000 t, worth US $1.6 billion. Of this, around 145,000 t of salmon and trout were produced in northern Norway, at a production (i.e., before sales) value of approximately US $470 million. This makes salmon the single most important species in terms of economic value, both in northern Norway and in the Norwegian fishing industry as a whole.

In 2000, there were 854 licenses for salmon and trout production in Norway, of which some 30% were for sites located in the three northern counties[38]. The number of plants and sites in northern Norway is expected to increase considerably in the future[39]. In addition to salmon, this development will also involve other fish species such as Atlantic halibut] (Hippoglossus hippoglossus) and cod. Over time, aquaculture is expected to become more important to the north Norwegian economy than the combined marine fisheries.

An important aspect of the aquaculture industry is that it is dependent on a huge supply of pelagic fish species. Fishmeal and oils are important components of the diet of many species of farmed fish, including salmon and trout. The quantity needed is so high that the industry at a global level is sensitive to rapid fluctuations in important pelagic stocks. El Niño–Southern Oscillation (ENSO) events in the Pacific have already affected the industry through impacts on anchovy (Engraulis spp.) stocks. From 1997 to 1998, the global marine fishery was reduced by nearly 8 million t, mainly due to ENSO events[40]. Reduced supply on the international market led to increased prices of fishmeal in this period. The latest assessment by the Intergovernmental Panel on Climate Change (Intergovernmental Panel on Climate Change (IPCC))[41] states that unless alternative sources of protein are found, aquaculture could in the future be limited by the supply of fishmeal and oils.

Aquaculture is in its infancy in northwest Russia and the total production is negligible. It is however likely to increase in the future.

Employment in the fisheries sector and the fisheries communities

There are approximately 17,000 fishers in Norway, of which almost half live in the three northern counties. In northern Norway it is common to combine fishing with other trades to make a living, particularly in remote areas. Part-time fishers make up about a third of the total number of people in the profession. The number of fishers has been sharply reduced over recent decades. This reflects broader societal changes with a shift in the workforce from primary to secondary and tertiary occupations, as well as technological development in the industry. A total of 12,420 persons worked in fish processing in Norway in 2000[42]. About half of these worked in the northernmost counties.

In 2001, around 3,600 people worked in aquaculture in Norway[43]. Of these about a third worked in the three northernmost counties. The combined direct employment in the fisheries sector in northern Norway is 16,000 to 17,000 people. The fisheries also generate substantial employment in related activities, such as shipbuilding, ship repairs, and gear production, as well as sales and exports. The number of people employed in the related industries has increased substantially over recent decades. The employment generated in related industries by the fisheries sector is 0.75 man-years per year in the fisheries[44], amounting to some 12,000 people in northern Norway. The total employment generated is therefore close to 30,000 people. With a total population in northern Norway of 460,000, this implies that the fisheries are crucial to employment and income in the region.

Corresponding data on employment in the fisheries sector for northwest Russia were not available.

According to Lindkvist[45] there are 96 communities in Norway that can be characterized as fishing communities. Of these, 42 occur in the three northern counties. Of these, 31 may be defined as fisheries-dependent in the sense that more than 5% of the working population is employed in fisheries and fish processing[46]. These communities are typically small and located in remote areas. Most face depopulation and problems such as lack of qualified personnel to maintain public services, but at the same time have few alternative trades to fishing. In Finnmark county, about 10% of the total employment is in the fisheries sector[47]. Remote, fisheries-dependent communities in northern Norway have the highest depopulation rates in the country. Since the 1980s, none of its municipalities have increased in population. On average the coastal municipalities have experienced a population reduction of around 30%[48].

Demographic pressure towards urbanization, which is expected to continue[49], may be said to be one of the major driving forces behind this development. Other factors, such as lack of employment opportunities and inferior public services, may be seen both as a cause of the problem as well as a consequence. There is also the trend of fishing boats being sold out of the communities. These trends indicate that the small fishery-dependent societies are under continuous pressure. These societies are subject to a “double exposure”[50], where climate change occurs simultaneously with economic marginalization. The Norwegian government has for a long period run programs aimed at strengthening the viability of fishery-dependent societies in the north. In recent years these efforts have been directed towards market orientation, flexibility, and a more robust industrial structure, rather than towards subsidies to the industry. Some [[region]al] development programs are aimed at diversification of the economic activity in remote areas by supporting, among other things, female-run enterprises[51].

Among the Russian Federation subjects in the northwest, the Murmansk Oblast is most important from the point of view of fisheries. This region is one of the most urbanized in Russia, with around 92% of the population living in cities and towns. Most of the northwest Russian fishing fleet is concentrated in the city of Murmansk. Some companies are located in the three other Russian Federation subjects: Arkhangelsk (Arkhangelsk Oblast), Petrozavodsk (Republic of Karelia), and Narjan-Mar (Nenets Autonomous Okrug).

The fishing industry is important for several major cities in northwestern Russia, but these cannot be characterized as “fishing communities” in the sense that this concept is understood in the West. Their viability is not dependent on fisheries. Also, the significance of the fishing industry has been severely reduced in the post-Soviet period as the catches of Russian vessels are mainly delivered to the West. The redirection of landings to the home market has been one of the main ambitions of Russian fishery authorities at both the federal and [[region]al] level since the early 1990s. That this has not been achieved points to the relative impotency of these bodies. At the federal level, the State Committee for Fisheries has twice lost its status as an independent body of governance (subsumed into the Ministry of Agriculture in 1992–1993 and 1997–1998) and seen its traditional all-embracing influence over fisheries management significantly reduced. In 2000, the Ministry of Trade and Economic Development succeeded in introducing a system for quota auctions, against the will of the State Committee for Fisheries. Regional authorities increased their influence during the 1990s. This development has now been reversed owing to the recentralization that began around 2000, commensurate with wider developments in Russia since President Putin came to power. Hence, while regional authorities in northwestern Russia have a declared aim of developing coastal fisheries, actual development in this sphere can only be considered minimal.

Markets

All data in this section are from the Norwegian Seafood Export Council.

Norway is one of the worlds biggest fish exporters – more than 90% of the landings are exported (in 2001 Norway was the world’s second largest fish exporter, after Thailand). There are two aspects to this. First, the income generated by fish exports is substantial – around US $4 billion in 2001. As the production in aquaculture will increase, and the production of petroleum will decrease, exports of fish products can be expected to become more important in the future. The Ministry of Fisheries envisages that aquaculture will become a mainstay of the Norwegian economy in the years to come, and that the sales value in northern Norway will be nearly five times higher in 2020 than today. Second, Norway is a major supplier to many [[market]s]. The Norwegian imports are important to, for example, the EU market for seafood, which is therefore vulnerable to fluctuations in Norwegian fisheries.

The single most important species in terms of export value is salmon which had an export value of US $1.8 billion in 2000. The second most important category is whitefish, the exports of which (consisting mainly of cod, haddock, and saithe) are worth in the range of US $1.2 billion annually. Pelagic species, of which herring is the most important, had an export value of US $920 million in 2001. The fourth most important species in terms of export value is northern shrimp.

Landings of Russian-caught cod in Norway have increased since 1990. During 1995 to 1997, landings were around 250,000 to 300,000t per year. Since then, there has been a reduction in Russian landings of cod as well as other fish in Norway. Trans-shipments of fish at sea and landings in other countries are increasing while landings in Norway are decreasing. Catches landed in Russia mostly go to the Russian consumer market. Imports of fish to Russia from Norway are rapidly increasing.

The management regime

In addition to the EEZ, Norway also manages the resources in the Fishery Zone around Jan Mayen and in the Fishery Protection Zone around Svalbard. The Norwegian EEZ borders the EU zone to the south, the Faroe Islands to the southwest, and Russia to the east. A large area beyond the EEZ boundary in the Norwegian Sea and a smaller area in the Barents Sea are international waters. Most of the economically important stocks move between the zones of two or more states.

Cooperation between the owner countries in the management of these stocks is essential to ensure their sustainable use. A series of agreements has been negotiated among the countries in the Northeast Atlantic that establish bilateral and multilateral arrangements for cooperation on fisheries management. The most extensive management regime on arctic stocks in the Northeast Atlantic is that between Norway and Russia. A joint fisheries commission meets annually to agree on TACs and the allocation for the major fisheries in the Barents Sea: i.e., those for cod, haddock, and capelin (since 2001 a total quota has also been set for the king crab fishery). The total quotas set are shared between the two countries – the allocation key is 50-50 for cod and haddock, and 60-40 for capelin. A fixed additional quantity is traded to third countries. There are also agreements on mutual access to the EEZs and exchange of quotas through this arrangement[52]. An important aspect of the cooperation with Russia is that a substantial part of the Russian harvest in the Barents Sea is taken in the Norwegian zone and landed in Norway. The cooperation also entails joint efforts in fisheries research and in enforcement of fisheries regulations.

Despite disagreement between Norway and Russia on the delimitation of the boundary between their EEZ and the shelf in the Barents Sea, the cooperation on resource management between the two countries may generally be characterized as well functioning[53]. However, agreed TACs by Norway and Russia have, in some years, exceeded those recommended by fisheries scientists. In addition, the actual catches have sometimes been larger than those agreed. Since the late 1990s, a precautionary approach has been gradually implemented in the management of the most important fisheries. However, retrospective analyses have shown that ICES estimates of stock sizes have often been too high, thereby incorrectly estimating the effect of a proposed regulatory measure on the stock. This has had the unfortunate effect that stock sizes for a given year are adjusted downward in subsequent assessments, rendering adopted management strategies ineffective[54]. However, the Joint Norwegian–Russian Fisheries Commission has decided that from 2004 onward multi-annual quotas based on a precautionary approach will be applied. A new management strategy adopted in 2003 shall ensure that TACs for any three-year period shall be in line with the precautionary reference values provided by ICES.

A number of other agreements are also in effect in the area, notably a five-party agreement among the coastal states in the Northeast Atlantic to manage Atlanto-Scandian herring[55]. Total quotas for the following year’s herring fishery are set, and divided among the parties. A separate quota is set for the area on the high seas in the Norwegian Sea. The high-seas quota, most of which is given to the same coastal states, is formally managed by the NEAFC (North East Atlantic Fisheries Commission), which is mandated to manage the fishing on the high seas in the Northeast Atlantic. Norway also has an extensive cooperation with the EU on the management of shared stocks in the North Sea (North Sea, Europe), as well as on the exchange of fish quotas, which entails access for EU vessels to north Norwegian waters. The EU is given a major share of the third country quota of cod in the Norwegian waters north of 62º N.

Management measures for marine mammals harvested in the area are decided by the IWC (International Whaling Commission), NAMMCO (North Atlantic Marine Mammal Commission), and the Joint Norwegian–Russian Fisheries Commission. The IWC has not been able to adopt a Revised Management Scheme and so does not set quotas. Since 1993, Norway has set unilateral quotas for the take of minke whales, on the basis of the work of the IWC Scientific Committee[56]. NAMMCO adopts management measures for cetaceans and seals in the northern Northeast Atlantic[57].

A precondition for sound management of living marine resources is that sufficient knowledge about the resources is available. In Norway, the Institute of Marine Research is the main governmental research institution, while the Northern Institute of Marine Research (PINRO) plays the same role on the Russian side. ICES is the international institution for formulating scientific advice to the fisheries authorities in the North Atlantic countries. Its work is generally based on inputs from the research institutions in the member countries. The ICES advice is now based on a precautionary approach, which seeks to introduce a greater sensitivity to risk and uncertainty into management. Three of the challenges for fisheries management in the future are: a better understanding of species interactions (multi-species management), more reliable data from scientific surveys, and a better understanding of the impact of physical factors – such as changing climatic conditions – on stocks. A major challenge is the development and implementation of an ecosystem-based approach to the management of living marine resources, where the effects of climate change are also considered when establishing management measures.

The management measures essentially fall into three categories:

- input regulations in the form of licensing schemes restricting access to a fishery;

- output regulations, consisting of the fish quotas given to various groups of fishers which limit the amount of fish they are entitled to in any given season; and

- technical measures specifying for example the type of fishing gear to be used in a particular fishery.

The objectives of fisheries management in Norway are related to conservation, efficiency, and [[region]al] considerations[58]. Conservation of resources is seen as a precondition for the development of an efficient industry and maintenance of viable fishing communities. An important objective of the fisheries policy is to improve the economic efficiency of the industry. An important issue is therefore to reduce the capacity of the fishing fleet, which is much larger than needed to take the quotas available and therefore makes the costs of fishing too high. Attempts to remove excess capacity include scrapping of vessels, regulatory mechanisms, and vessel construction regulations. A quota arrangement allowing for merging two vessels’ quotas while removing one of the vessels from the fishery gives vessel owners an incentive to remove excess fishing capacity, and can contribute to a more efficient fleet. However, this can result in coastal communities seeing their local fleet reduced or even disappearing, threatening the viability of that community.

The enforcement of the fisheries regulations in Norway is carried out both at sea and when the fish is landed. At sea, the Coast Guard is responsible for inspecting fishing vessels and checking their catch against vessel logbooks. Foreign vessels fishing in Norwegian waters are also inspected. The activity of the Coast Guard is vital for the functioning of the management regime as a whole. Ocean-going vessels are required to install and use a satellite-based vessel-monitoring system enabling the authorities to continually monitor their activities. The Directorate of Fisheries also inspects activities on the fishing grounds, as well as at the landing sites. When fish is landed, the sales organization buying the fish reports the landed quantity to the Fisheries Directorate, which is responsible for maintaining the fisheries statistics.

The regulation of Soviet fisheries in the Northeast Atlantic used to be the responsibility of the Sevryba association. As this organization lost its status in fisheries regulation in the mid-1990s, the regulatory tasks were partly taken over by the enforcement body Murmanrybvod, partly by the fisheries departments of regional authorities in each federal subject in the area, and since 2000 to an increasing extent the regulatory tasks have been the remit of federal authorities. During the 1990s, the Russian share of the Barents Sea quotas was first divided among the four federal subjects of the region by the so-called Scientific Catch Council (formerly headed by Sevryba, since 2001 by the federal State Committee for Fisheries). Within each federal subject, a Fisheries Council (led by regional authorities) distributed quota shares among individual ship owners. The influence of both the Scientific Catch Council and the regional Fisheries Councils was reduced after the introduction of quota auctions in 2000/2001. Since then, an increasing share of the quotas has been sold at auctions, administered by the federal Ministry of Trade and Economic Development. In November 2003, the Russian Government decided to abolish the auctions and instead introduce a resource rent (a fee on quota shares). The quotas will from 2004 be distributed by an inter-ministerial commission at the federal level, so the regional authorities will also lose the influence of interregional quota allocation[59].

Apart from quotas, the Russians have fishery regulations similar to those in the Norwegian system: regulations pertaining to fishing gear, size of the fish, and composition of individual catches. In addition, the Russians have a more fine-meshed system than the Norwegians for closing and opening of fishing grounds. Individual inspectors from the enforcement body Murmanrybvod or researchers from the scientific institute PINRO can close a “rectangle” (a square nautical mile) on site for a period of three days. After three days, the “rectangle” is reopened if scientists make no objections, i.e., if the proportion of undersized fish in catches does not continue to exceed legal limits.

Traditionally, the civilian fishery inspection service Murmanrybvod, subordinate to the Russian State Committee for Fisheries, has been responsible for enforcing Russian fishery regulations in the Barents Sea. In 1998, responsibility for fisheries enforcement at sea in the Russian Federation was transferred to the Federal Border Service. In the northern fishery basin, the Murmansk State Inspection of the Arctic Regional Command of the Federal Border Service was established to take care of fisheries enforcement. However, this body is only responsible for physical inspections at sea, while inspection of landed catches has been transferred to the Border Guard. Murmanrybvod is still in charge of keeping track of how much of the quotas has been caught by individual ship owners at any one time. It has also retained its responsibility for the closing of fishing grounds in areas with excessive intermingling of undersized fish, a very important regulatory measure in both the Russian and Norwegian part of the Barents Sea. Finally, Murmanrybvod is still responsible for enforcement in international convention areas. In practice, Murmanrybvod places its inspectors on board northwest Russian fishing vessels that fish in the NEAFC or NAFO areas.

The reorganization of the Russian enforcement system is generally believed to have led to a reduction in the system’s effectiveness, at least from a short-term perspective. For example, officers in the Murmansk State Inspection of the Federal Border Service generally lack experience in fisheries management and enforcement. This has partly been compensated for by the transfer of some of Murmanrybvod’s inspectors. More apparent is the lack of material resources to maintain a presence at sea. Contrary to the intentions of the reorganization of the enforcement system, the presence at sea by [[monitor]ing] vessels has declined since the Border Guard took over this duty in 1998. Precise data for presence at sea and inspection frequency are not available, but Jørgensen[60] estimated that the Border Guard performed around 160 inspections at sea in 1998, which represents a significant reduction compared to an estimated 700 to 1000 annual inspections at sea by Murmanrybvod prior to the reorganization. For periods of several months during 1998, not a single enforcement vessel was present on the fishing grounds in the Russian part of the Barents Sea. Officials of the Border Service explain this by a lack of funds to purchase fuel. Critics question the genuineness of the Border Service’s will to play a role in fisheries management. The result of the reorganization has, in any event, so far led to a tangible reduction in the effectiveness of Russian enforcement in the Barents Sea.

Economic and social impacts of climate change on fisheries in the Northeast Atlantic (13.2.6)

The economic importance of fisheries to northern Norway is substantial, cod being the most significant species. Problems related to profitability in the fishing industry have been evident for a long time, and have contributed to depopulation problems in remote, fishery dependent areas. Aquaculture is, however, a growing industry and is expected to be important to the future viability of local communities in northern Norway. In northwest Russia, the fishing industry is based in big cities, Murmansk in particular, and is therefore not as significant to local communities as it is in Norway.

A study by Furevik et al.[61] developing regional ocean surface temperature scenarios for the Northeast Atlantic concluded that for the 2020 scenario, no substantial change is likely in the physical parameters. The authors concluded that a slight cooling in ocean surface temperature is likely by 2020 with warming likely in the longer-term scenarios. For the near-term future, climate change is therefore not likely to have a major impact on the fisheries in the region. Uncertainties surrounding these scenarios are however considerable. These are amplified when the physical effects on biota are included, and amplified again when the effects of climate change on society are added. In addition, social change is driven by a vast number of factors, of which climate change is only one. The rest of this section is therefore tentative and should be read more as discussions of likely patterns of change than predictions of future developments.

The effects of climate change are closely related to the vulnerability of industries and communities, and to their capability to adapt to change and mitigate the effects of change. Within this context vulnerability is defined as “the extent to which a natural or social system is susceptible to sustaining damage from climate change”[62]. It depends on the ability and capacity of society at the international, national, and regional level to cope with change and to remedy its negative effects. Climate change may also result in positive changes.

The fisheries sector is one in which the industry has always had to adapt to and cope with environmental change: the abundance of various species of fish and marine mammals has varied throughout history, often dramatically and also within short periods of time. Adapting to changing circumstances is therefore second nature to the fishing industry as well as to the communities that depend upon it. An important issue is thus whether climate change brings about changes at scales and rates that are unknown, and whether adaptation can be achieved within the existing institutional structures.

Resource management

Resource management is the key factor in deciding the biological and economic sustainability of the fisheries. The fishing opportunities are decided by the management regime. There are virtually no remaining fisheries where the economic result is decided by the industry itself. The design and operation of both the domestic and international management regimes are crucial to the sustainability and economic efficiency of the fisheries, and hence to the economic viability of the communities that depend upon them. The development and implementation of a precautionary approach, as well as the emergence of ecosystem-based management, may enhance the resilience of the stocks and therefore make the industry and communities more robust to future external shocks. As discussed in Section 7.7 (Fisheries and aquaculture in the Northeast Atlantic (Barents and Norwegian Seas)), the main arrangements for managing living marine resources in the Northeast Atlantic are being modified in this direction, with the implementation of a precautionary approach and the development of an ecosystem-based approach to management.

A major challenge for the management regime is that of adjusting to the possible changes in migration patterns of stocks resulting from climate change. This finding is in conformity with that of the IPCC[63] and Everett et al.[64]. Changes in migration patterns of fish stocks have previously upset established arrangements for resource management, and can trigger conflicts between countries. One example is that of northeast Atlantic cod: in the early 1990s, the stock extended its range northward in the Barents Sea, into the high seas in the area (the so-called “loophole”). Vessels from a number of countries without fishing rights in the cod fishery took the opportunity to initiate an unregulated fishery in the area, thereby undermining the Norwegian–Russian management regime. This triggered a conflict between Norway and Russia on the one hand, and Iceland on the other. The conflict was later resolved through a trilateral agreement[65]. Another example is that of the Norwegian spring-spawning herring: following more than two decades of effort at rebuilding the stock on the part of Norwegian authorities, in the mid-1990s the stock began to migrate from the Norwegian EEZ and into international waters for parts of the year. By doing so the stock became accessible to vessels from other countries, and in the absence of an effective management regime for the stock in the high seas, efforts at rebuilding the stock could prove futile. A regime securing a management scheme for the stock eventually came into place, but took several years to negotiate. Thus, changes in migration patterns, which are likely to be triggered by changes in water (Seawater) [[temperature]s], tend to result in unregulated fishing and conflicts among countries. The outcome of such conflicts may be conflicting management strategies, new distribution formulas, or even new management regimes.

Another important factor is that negative events tend to be a liability to the management regime. The so-called “cod crisis” in the late 1980s, for example, led to several modifications of the existing regime. The management regime is likely to be held responsible for social and economic consequences of climate change. This may in turn affect the legitimacy and authority of the regime, and its effectiveness in regulating the industry. An important aspect in that regard is the way decisions about resource management and allocation of resources are made. A regime that involves those interests that are affected by decisions in the decision-making processes tends to produce regulations that are considered more legitimate than regimes that do not involve stakeholders[66].

Current fisheries management models are mainly based on general assumptions of constant environmental factors. The current methods applied in fisheries management can not accommodate environmental changes. A study by Eide and Heen[67] investigated the economic output from the fisheries under different environmental scenarios and under different management regimes for the cod and capelin fisheries in the Barents Sea. Using the ECONMULT fleet model[68] and a regional impact model for the north Norwegian economy[69], they concluded that even a narrow range of management regimes has a variety of possible economic outcomes. Even though climate change may result in significant potential effects on catches, profitability, employment, and income, changes in the management regimes seem to have an even larger impact. This conclusion sets the discussion of effects of global climate change in perspective. It implies that a large number of factors influence the economic activities and their output and, furthermore, that the operation of the management regime seems to be the most significant of these factors.

The crucial factor for resource management under conditions of climate change is therefore the development of robust and precautionary approaches and institutions for managing the resources. The decisive factor for the health of fish stocks, and therefore the fate of the fishing industry and its dependent communities, appears to be the resource management regime.

The fishing fleet

The ability to adapt to changes in migration patterns or stock size of commercially exploited species will vary between different vessel groups in the fishing fleet. The ocean-going fleet is capable of adjusting to changes in migration patterns, as it has a wide operating range. Small coastal vessels are more limited in that regard. Thus, northern communities with a strong dependency on small coastal vessels are likely to be more affected if migration patterns and availability of important fish stocks change significantly. If fish stocks move closer to the coast it is an advantage to the coastal fleet, while it is a disadvantage for this fleet if the stocks move more seaward. Such a development may be confounded by changing weather patterns with severe weather events becoming more prevalent. All vessel groups will be affected if changes lead to stocks crossing jurisdictional borders. That may imply a change in distribution of resources among countries.

Increased production and larger stocks of cod and herring are possible outcomes of climate change in the Northeast Atlantic. A question arises as to which fleet groups are most capable of making the best of such positive changes in the resource. Such changes may result in different availability of the resources between groups of fisheries (e.g., coastal versus ocean-going vessels), affecting the domestic allocation of resources. It may also lead to a greater political pressure to change the allocation of resources between the main groups of resource users.

Changes in stock abundance and migration patterns are not new to the industry. The availability of fish stocks and their accessibility to the coastal fleet has changed throughout recorded history, and the industry as well as the management regime is used to adapting to changing circumstances. The key question is whether climate change would amplify such variations and aggravate their effects beyond the scale with which the industry and the regulating authorities are familiar.

Changes in oceanic conditions may also affect the migrating ranges of marine mammals, and hence marine mammal–fisheries interactions. Such interactions could include marine mammals preying on fish, thus increasing competition with fishers, or marine mammals interacting directly with the fishery, for example by interfering with fishing gear. Marine mammals are also vectors of parasites that may affect fish and fisheries.

Aquaculture

Higher water temperature generally has positive effects on aquaculture in terms of fish growth. The IPCC reported that warming and consequent lengthening of the growing season could have beneficial effects with respect to growth rates and feed conversion efficiency[70]. Warmer waters may also have negative effects on aquaculture since the presence of lice and diseases may be related to water temperature. In recent years high water temperatures in late summer have caused high mortality at farms rearing halibut and cod, the production of which is still at a pre-commercial stage. Salmon is also affected by high temperatures and farms may expect higher mortalities of salmon. A rise in sea temperatures may therefore favor a northward movement of production, to sites where the peak water (Seawater) temperatures are unlikely to be above levels at which fish become negatively affected.

An increase in severe weather events can be a cause of escapes from fish pens and consequent loss of production. Escapes are also a potential problem in terms of the spread of disease. However, technological developments may compensate for this.

The aquaculture industry is dependent on capture fish for salmon feed. Climate change may cause a lack of and/or variability in the market for such products, but this is also an area where research may lead to the development of other feed sources.

The processing industry, communities, and markets

The fish processing industry in the north faces challenges in the structural changes both in the first-hand market (from fisher to buyer) and in the export market. Increased international competition for scarce resources has left the processing side of the industry increasingly vulnerable to globalization pressures. At the same time many of the communities, depending on fisheries for their existence, experience economic marginalization and depopulation-related problems. The vulnerability of the fishing industry and fishing communities can therefore be considered as relatively high at the outset, rendering them particularly susceptible to any negative influences resulting from climate change. Such impacts may however be minor compared to that of other drivers of change. Furthermore, the fish processing industry is very varied. The size of fish processing plants is one aspect of this, their versatility and ability to vary production and adapt to changing circumstances is another. The ability of the particular type of industry to adapt to various earlier “crises”, whether in terms of demand or supply failures, could be an indicator of their future “coping-capacity” for effects resulting from climate change. Another issue is that climate-induced changes elsewhere in the world may affect the situation for the north Norwegian fishing industry and fishing communities. Experience from, for example, the fisheries crisis in Canada in the 1990s indicates that such situations tend to intensify competition for further processing of the raw material. To the industry in Norway, with high labor costs, such a scenario is negative.

Ability to cope with change (13.2.7)

Many factors contribute to a community’s “coping capacity” in relation to depopulation and to structural changes in the fisheries sector[71]. The future of these settlements may depend on their ability to adapt to increased competition, efficiency, deregulation, and liberalization of the [[market]s], as much as on the accessibility of fishing resources for their local production systems[72].

While the management regime can be seen as an instrument to ease negative effects of climate change, it is however also important to consider public measures beyond the fisheries management regime that affect the conditions of the fishing industry more broadly, as for example [[region]al] policies and the development of alternative means of employment. Measures for building infrastructure such as roads or to develop harbor facilities are but one example. Government support for fisheries in the form of direct subsidies is now effectively prohibited by international agreements. But in Norway in particular there is a strong tradition for supporting regional development in a broader sense, and programs to this end may enhance the resilience of northern communities.

In addition to adapting to possible changes in the resource resulting from climate change, the fishing communities will also need to adapt to possible other climate-related changes in their vicinity (e.g., weather events) and their effects on terrestrial biota and infrastructure. These may have indirect effects on the fishery sector, related economic activities, or on other aspects of life, valued by the people in the respective communities.

Concluding comments (13.2.8)