Total Cost

In economics, the total cost (TC) is the total economic cost of production. It consists of variable costs and fixed costs. Total cost is the total opportunity cost of each factor of production as part of its fixed or variable costs .

Calculating total cost

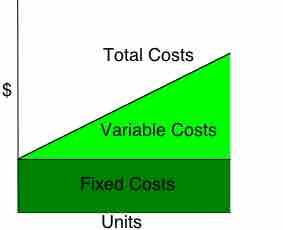

This graphs shows the relationship between fixed cost and variable cost. The sum of the two equal the total cost.

Variable Costs

Variable cost (VC) changes according to the quantity of a good or service being produced. It includes inputs like labor and raw materials. Variable costs are also the sum of marginal costs over all of the units produced (referred to as normal costs). For example, in the case of a clothing manufacturer, the variable costs would be the cost of the direct material (cloth) and the direct labor. The amount of materials and labor that is needed for each shirt increases in direct proportion to the number of shirts produced. The cost "varies" according to production.

Fixed Costs

Fixed costs (FC) are incurred independent of the quality of goods or services produced. They include inputs (capital) that cannot be adjusted in the short term, such as buildings and machinery. Fixed costs (also referred to as overhead costs) tend to be time related costs, including salaries or monthly rental fees. An example of a fixed cost would be the cost of renting a warehouse for a specific lease period. However, fixed costs are not permanent. They are only fixed in relation to the quantity of production for a certain time period. In the long run, the cost of all inputs is variable.

Economic Cost

The economic cost of a decision that a firm makes depends on the cost of the alternative chosen and the benefit that the best alternative would have provided if chosen. Economic cost is the sum of all the variable and fixed costs (also called accounting cost) plus opportunity costs.