Partnerships and Taxes

Different types of partnerships have different tax requirements, and partners will need to fill out different forms depending on the type. Below, we discuss Subchapter S Corporations, and LLCs.

Subchapter S Corporations

Subchapter S Corporations have a tax election only; this election enables the shareholder to treat the earnings and profits as distributions and have them pass through directly to their personal tax return. The catch here is that the shareholder, if working for the company (and if there is a profit), must pay him/herself wages, and must meet standards of "reasonable compensation". This can vary by geographical region as well as occupation, but the basic rule is to pay yourself what you would have to pay someone else to do your job, as long as there is enough profit. If you do not do this, the IRS can reclassify all of the earnings and profit as wages, and you will be liable for all of the payroll taxes on the total amount.

Limited Liability Company (LLC)

The LLC is a relatively new type of hybrid business structure that is now permissible in most states. It is designed to provide the limited liability features of a corporation and the tax efficiencies and operational flexibility of a partnership. Formation is more complex and formal than that of a general partnership. The owners are members, and the duration of the LLC is usually determined when the organization papers are filed. The time limit can be continued, if desired, by a vote of the members at the time of expiration. LLCs must not have more than two of the four characteristics that define corporations: Limited liability to the extent of assets, continuity of life, centralization of management, and free transferability of ownership interests.

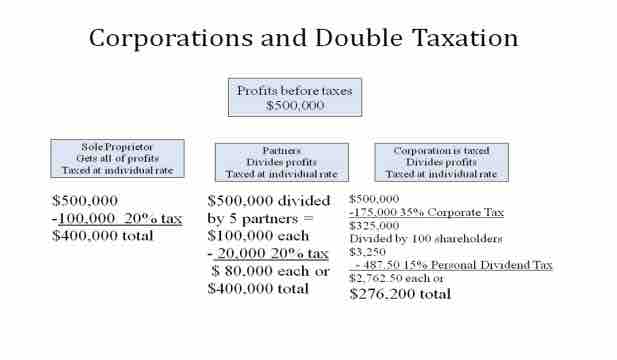

Corporations and Double Taxation

This figure shows how corporations are taxed twice.