Intermediate Equipment Handbook

Intech Associates

economic life of 10,000 engine hours. The difference between the cost new and

the residual/scrap value should be spread over the anticipated 10,000 hour

working life and charged to the user for each hour used. The economic life or

asset value of the piece of equipment is being consumed and should be paid

for.

Naturally if the economic life is assessed to be only 5,000 hours for various

reasons then the depreciation charges should be adjusted accordingly, i.e.

double in this case. It is therefore very important that the owner is realistic in

his/her assessment of the economic life. The factors indicated in Figure 1.1 are

influential in the determination of this. Economic life can vary by a factor of more

than 10 under the range of influences in practice.

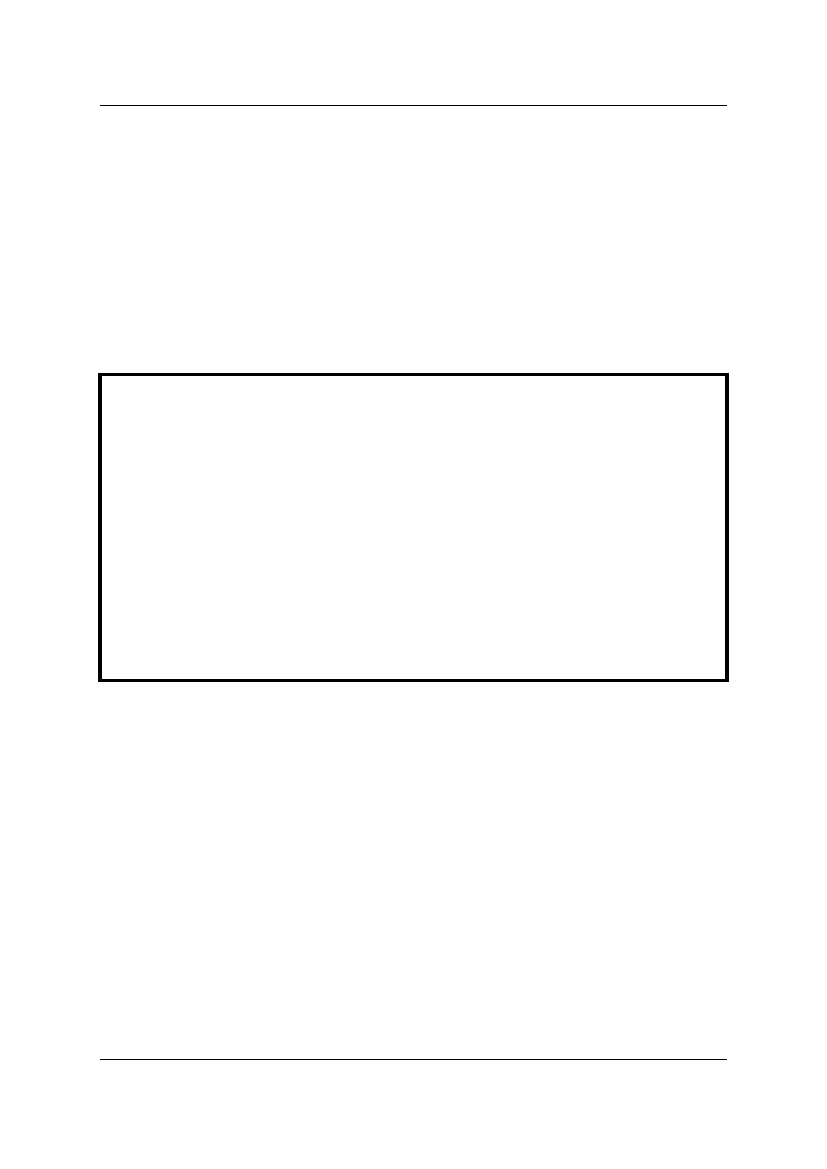

Figure 1.2 Case Study - Effect of Equipment Life on Depreciation

Charges

A piece of equipment costs 150,000 Local Currency Units (LCU). It is assumed

that at the end of its life it has no residual or scrap value.

If it works for its total design life of 10,000 hours, the depreciation cost would be

15 LCU/hour.

If it works only half its design life (5,000 hours) before being scrapped, the

depreciation cost would be 30 LCU/hour.

If it works only 1,000 hours before being scrapped, the depreciation cost would

be 150 LCU/hour.

It is important to appreciate that even with inflation the residual value is always

tending towards zero or a very small value (unlike say, an investment in prime

property).

If there is significant inflation, as is experienced in many developing countries,

then it is important to regularly revise depreciation charge rates to reflect current

replacement costs of the equipment. Otherwise the value of asset being used

up will be undervalued and insufficient funds will be raised to replace the asset

or repay the capital investment. Continuing with the example above, each hour

of an expected 10,000 hour life should be charged at 1/10,000th of the current

difference between cost new and scrap to avoid loss of asset value.

October 2012

32